February 17, 2026

Iran: Food Import Policy Shift and Grain Trade Outlook (2026)

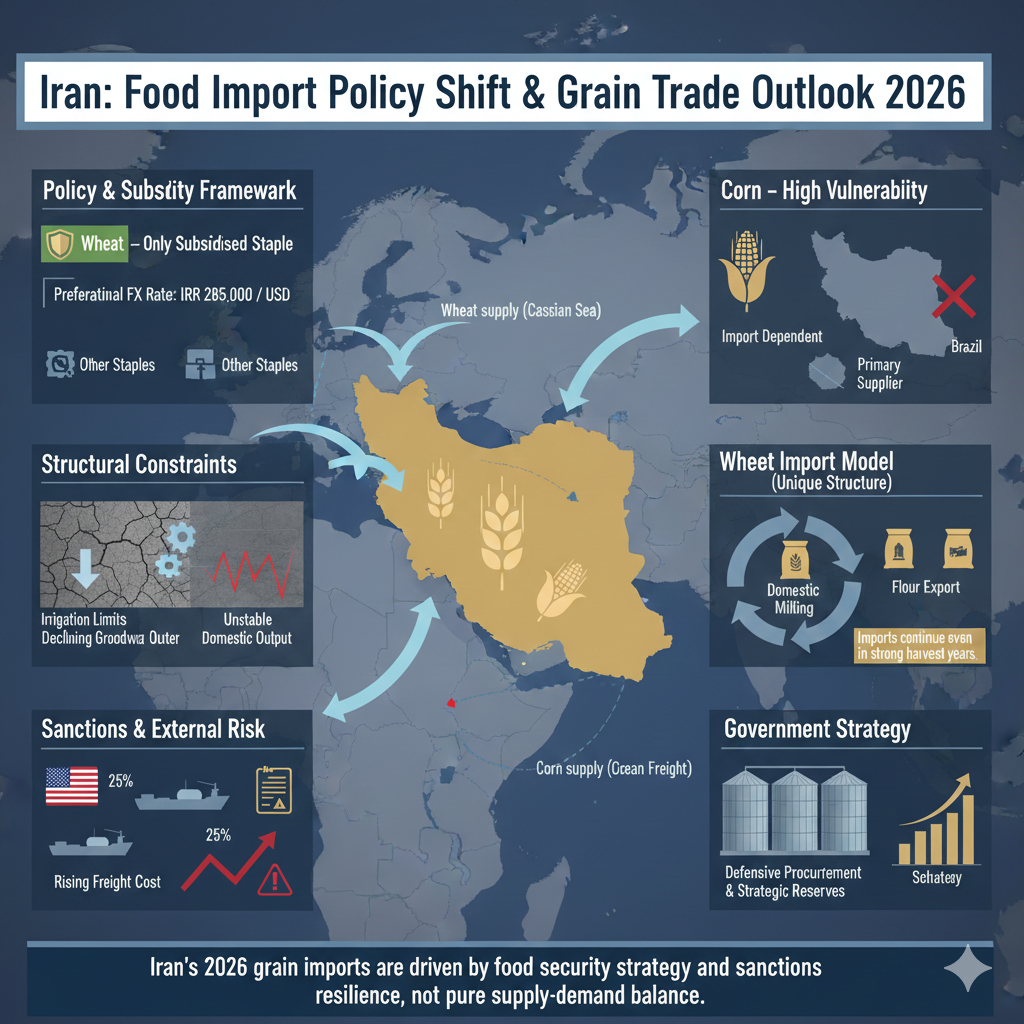

Policy Framework and Subsidy Regime

In 2026, Iran has significantly tightened its food import subsidy regime. The government has removed subsidies for all staple food imports except wheat, positioning wheat as the core pillar of national food security. The Ministry of Agriculture Jihad (MAJ) will continue to subsidise wheat imports through a preferential exchange rate of IRR 285,000 per USD, ensuring price stability for bread and flour—politically and socially sensitive commodities.

This policy shift reflects Iran’s broader macroeconomic pressures, including persistent inflation, currency volatility, and restricted access to foreign exchange.

Food Security Imperative

With a population exceeding 88 million and continuing to grow, food security has become Iran’s most critical strategic objective. Structural economic uncertainty, compounded by international sanctions, has forced the government to prioritise availability over efficiency, even at elevated fiscal cost.

Domestic Production vs. Structural Constraints

Iran continues to pursue self-sufficiency in key grains—wheat, barley, corn, and rice—under its long-standing “resistance economy” doctrine. However, this ambition faces severe constraints:

Chronic drought conditions, now extending into a sixth consecutive year

Severe water scarcity, limiting irrigation capacity

Declining groundwater reserves and rising production costs

As a result, domestic grain output remains highly volatile, preventing reliable substitution of imports.

Wheat: A特殊 Import Model

Iran’s wheat import dynamics remain structurally unique:

Even in years when domestic wheat production meets internal consumption, imports may still increase.

The government restricts the use of domestically produced wheat for flour exports.

To sustain flour exports to neighboring countries, Iran relies on imported wheat, which is milled domestically and then re-exported as flour.

This policy framework means that comfortable national wheat balances do not necessarily translate into lower imports.

Base-Case 2026 Wheat Supply

Core suppliers: Russia and Kazakhstan

Logistics advantage: Caspian Sea routes and overland corridors

Trade facilitation: EAEU-linked payment mechanisms and regional clearing formats

These origins are expected to dominate due to pricing competitiveness, political alignment, and sanction-resilient logistics.

Corn: The Most Vulnerable Segment

Unlike wheat, corn imports are structurally unavoidable:

Domestic corn production is severely constrained by water scarcity

Feed demand from Iran’s poultry and livestock sectors remains robust

Corn imports are highly sensitive to FX availability and macro conditions

Before 2022, Ukraine was a key supplier. However:

By 2026, Ukrainian exports to Iran are officially prohibited

Brazil has emerged as the dominant supplier

Russian corn exports remain irregular and opportunistic, constrained by quality, logistics, and policy volatility

Sanctions Risk and Strategic Stockpiling

The external risk environment has deteriorated further:

The United States has imposed new sanctions targeting Iran’s “shadow fleet”, used primarily for oil exports

President Trump has publicly warned of a potential 25% tariff on all US imports from countries continuing commercial engagement with Iran

These developments raise the risk of:

Tighter shipping insurance

Reduced trade finance availability

Higher transaction and freight costs

Government Response: Pre-emptive Procurement

In anticipation of a potential tightening of the economic blockade, Iranian authorities are actively:

Accelerating government-led grain purchases

Building strategic food reserves

Prioritising volumes and security of supply over price optimisation

This stockpiling behavior is expected to support import demand in 2026, even during periods of relative domestic supply comfort.

Trade Outlook Summary (2026)

Wheat: Subsidised, politically protected, structurally imported regardless of crop size

Corn: Fully import-dependent, highly sensitive, Brazil-led supply

Suppliers: Russia, Kazakhstan, and Brazil remain best positioned

Market behavior: Defensive procurement, stock accumulation, sanction-resilient logistics

Bottom line: Iran’s grain imports in 2026 are driven less by pure supply-demand balance and more by sanctions risk, logistics access, and food security strategy, ensuring continued presence in global grain trade despite mounting external pressures